Liberty Mutual spends a lot of money making sure you know its name. Between the ubiquitous “only pay for what you need” commercials and its sponsorship presence across sports broadcasts, it’s one of the most recognizable insurance brands in the country. What the ads don’t tell you is what actually happens after you sign the policy, so I went looking for that story instead, digging through complaint databases, third-party ratings, and hundreds of customer reviews to see whether the reputation matches the reality.

What emerged wasn’t a simple thumbs up or thumbs down. It was a more specific pattern: a company that performs well on paper, in terms of financial strength and coverage breadth, but generates a disproportionate amount of frustration once customers actually need to use their policy or watch their premium change over time.

Here’s what the data, and the customers, actually say.

The Basics: Who Is Liberty Mutual?

Liberty Mutual is one of the largest property and casualty insurers in the world, founded in 1912 and headquartered in Boston. It operates as a mutual company, meaning U.S. policyholders are technically considered part-owners rather than shareholders answering to outside investors, a structure it shares with companies like State Farm and USAA. By premium volume, it ranks among the largest insurers globally, and it holds a position within the Fortune 100 based on recent revenue figures.

The company offers a wide product lineup, including auto, home, renters, condo, umbrella, life, pet, and various specialty and commercial insurance products. It’s worth noting that Liberty Mutual has announced plans to consolidate its personal insurance lines under a single brand name, meaning its longtime subsidiary Safeco is being phased out, with existing Safeco customers transitioning to Liberty Mutual policies without any change to their coverage or agent.

Financial Strength: The One Category Where It’s Nearly Unanimous

If there’s one area where reviewers and rating agencies agree without much argument, it’s financial stability. AM Best, the primary rating agency for insurance company solvency, rates Liberty Mutual in its “Excellent” tier, reflecting a strong ability to pay out claims even during periods of heavy losses. For a company this size, insuring millions of policyholders across auto, home, and commercial lines, that’s a meaningful data point. Whatever else this review has to say about customer experience, the company isn’t at risk of failing to honor claims due to its own financial instability.

Pricing: Reasonably Competitive, With a Catch

Here’s where things get more complicated, and where reviewers seem to split the most sharply.

Liberty Mutual doesn’t publish its rate filings the way some competitors do, which makes direct national comparisons difficult. Independent insurance comparison sites report noticeably different average premium figures, depending on their sampling and methodology, generally placing Liberty Mutual’s typical auto premiums above the national average, though not dramatically out of line with other major national carriers.

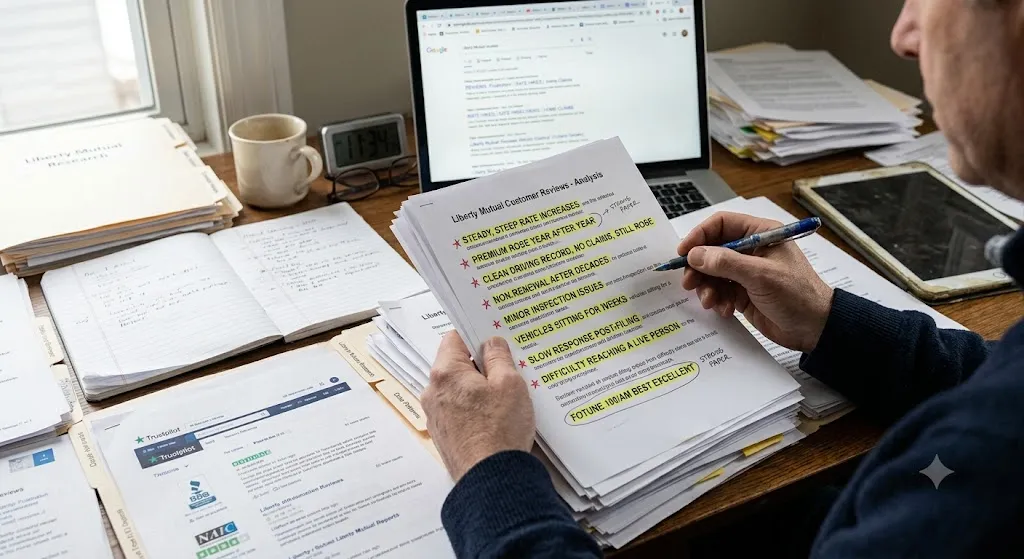

The bigger issue that shows up consistently across reviews isn’t the starting price. It’s what happens after. A recurring theme across Trustpilot, the Better Business Bureau, and consumer review platforms is customers reporting steady, sometimes steep, rate increases at renewal, often despite a clean driving record, no new claims, and no changes in circumstances. Several reviewers describe premiums that rose year after year until the cost simply became difficult to justify next to a competitor’s quote. This isn’t unique to Liberty Mutual; renewal creep is a well-documented industry-wide frustration. But it comes up often enough in Liberty Mutual-specific reviews that it’s worth flagging as a genuine pattern rather than a handful of isolated complaints.

The takeaway for prospective customers: an attractive initial quote doesn’t necessarily predict what you’ll be paying two or three renewal cycles later. Shopping your policy periodically, rather than assuming loyalty will be rewarded with stable pricing, seems to be the most consistent advice embedded in the reviews themselves.

Discounts and the RightTrack Program

To its credit, Liberty Mutual offers a genuinely broad discount lineup, including the usual multi-policy and continuous-coverage discounts, along with its RightTrack telematics program. RightTrack tracks driving behavior through a mobile app or plug-in device and offers an upfront discount just for enrolling, with the potential for a larger final discount, reportedly up to 30 percent, based on demonstrated safe driving habits. One notable detail: Liberty Mutual states that RightTrack will not increase your rate even if it detects poor driving habits, which distinguishes it from some competing telematics programs that can raise prices based on tracked behavior.

For homeowners, available discounts include reductions for staying claims-free over multiple years, insuring your home for its full replacement cost, enrolling in automatic payments, and even credits for wind mitigation improvements or a newly installed roof. Bundling home and auto policies together is also commonly cited as one of the more reliable ways to lower overall costs with this insurer.

Claims Experience: The Most Polarizing Category

This is where Liberty Mutual’s reviews diverge most dramatically, and it’s the category worth paying closest attention to if you’re evaluating whether to buy a policy.

On one side, a meaningful number of reviewers describe fast, professional claims handling, particularly for straightforward auto accidents, citing quick rental car arrangements and responsive adjusters. Liberty Mutual has also received an above-average score in J.D. Power’s property claims satisfaction research, suggesting the claims experience can genuinely be a strength under the right circumstances.

On the other side, a substantial portion of negative reviews center specifically on claims, not everyday service. Common complaints include slow response times after filing, vehicles sitting at storage facilities for weeks awaiting a total-loss determination, and homeowners describing non-renewal of long-standing policies following a routine exterior inspection, sometimes citing minor issues like stored materials in a yard or cosmetic paint wear as justification. Several homeowners describe decades-long, claims-free relationships with the company ending abruptly over what they characterize as a minor or disputable inspection finding.

Independent complaint tracking backs up the sense that this is a real pattern rather than just louder-than-average unhappy customers. The National Association of Insurance Commissioners’ complaint index, which measures how many complaints a company generates relative to its size, has shown Liberty Mutual trending upward in recent years for auto insurance specifically, moving from a lower complaint ratio in 2023 to a noticeably higher one in 2024, according to analysis from multiple insurance research sites. That means Liberty Mutual is generating more complaints per policyholder than would be expected for a company of its size, and the trend has been heading in the wrong direction rather than improving.

Customer Service and Digital Tools

Reviewers are generally more positive about day-to-day customer service than about the claims process specifically. Liberty Mutual’s mobile app receives consistent praise for ease of use, bill payment, and policy management, and several reviewers describe helpful, knowledgeable agents for routine account questions. The friction seems to concentrate specifically around two moments: renewal pricing surprises, and the claims process itself, rather than everyday account servicing.

That said, it’s not universally smooth. A meaningful number of reviews describe difficulty reaching a live person for anything beyond basic account tasks, particularly when an assigned agent is unavailable, along with frustration from customers who feel steered toward self-service tools when they’d prefer direct agent support.

What the Ratings Organizations Say, Side by Side

Pulling together third-party assessments, a consistent shape emerges: strong marks for financial stability and coverage breadth, average-to-below-average marks for customer satisfaction and complaint volume. Consumer research firms have given Liberty Mutual middling-to-low overall scores specifically because of its complaint history, even while acknowledging competitive pricing and a wide range of coverage options. One prominent insurance research and ranking publication has gone as far as excluding Liberty Mutual from its “best homeowners insurance” rankings specifically due to persistently low consumer survey scores, despite the company’s scale and financial strength.

Should You Buy a Liberty Mutual Policy?

Based on everything above, a few honest conclusions seem fair:

Liberty Mutual is financially strong and unlikely to have solvency issues that would prevent it from paying a valid claim. It offers a genuinely wide range of coverage types and discount opportunities, and its digital tools are generally well-regarded. If your driving record and profile qualify you for a strong initial quote, and especially if you’re interested in the RightTrack telematics discount, it’s a reasonable option to get a quote from.

Where the company appears weaker, based on the volume and consistency of complaints, is in the experience of actually filing a claim, particularly for homeowners facing a non-renewal after an inspection, and in the predictability of pricing over time. Anyone considering Liberty Mutual should go in with clear eyes about both of those risks, shop the policy again at each renewal rather than assuming the price will stay competitive, and read the specific terms around home inspections and renewal conditions before signing.

As with any insurance decision, this article is meant to inform, not to recommend for or against a specific purchase. Insurance needs, driving records, home conditions, and state regulations vary enormously from one person to the next, and the best way to know whether Liberty Mutual, or any insurer, is right for you is to request a personalized quote and compare it directly against two or three competitors in your specific market.

Related posts:

Essential Metrics to Evaluate Before Investing in Oil

Essential Metrics to Evaluate Before Investing in Oil

How to Maximize Employee Motivation with Branded Reward Cards

How to Maximize Employee Motivation with Branded Reward Cards

Why Your Business Needs a Strong Mission Statement

Why Your Business Needs a Strong Mission Statement

How Verified Consultants Can Help You Close Office Deals Faster in Bangalore

How Verified Consultants Can Help You Close Office Deals Faster in Bangalore

How Maya Thompson Turned $100 Into a Million-Dollar Empire

How Maya Thompson Turned $100 Into a Million-Dollar Empire

Leave a Reply