The Stack of Lumber That Ended a 22-Year Policy: What Liberty Mutual’s Home Insurance Reviews Actually Reveal

There’s a specific kind of complaint that shows up again and again in Liberty Mutual’s homeowners insurance reviews, and it’s not about price, at least not directly. It’s about an inspector.

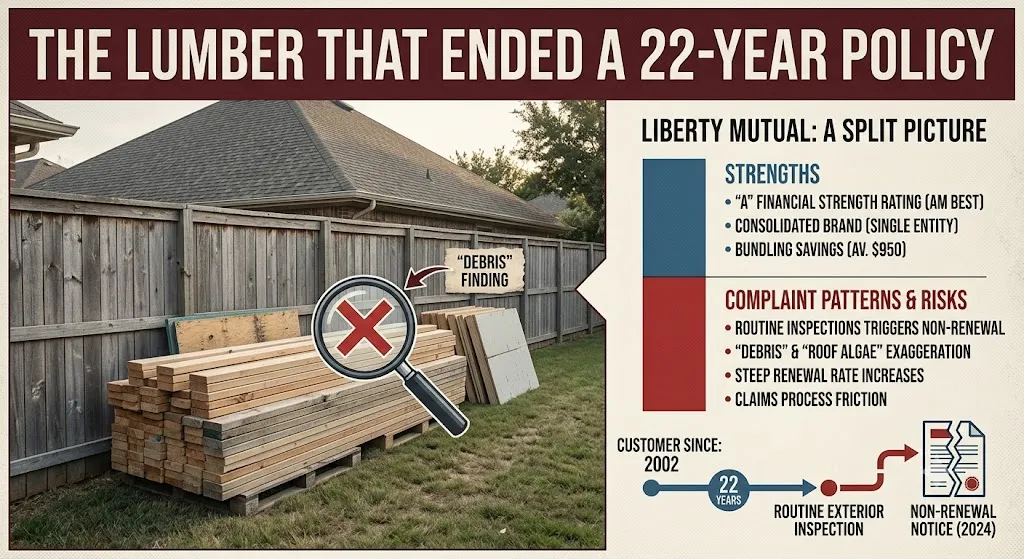

One Better Business Bureau review describes a customer of 22 years, two homes and two vehicles insured, never a missed payment, who lost her homeowners policy after a routine exterior inspection flagged neatly stacked lumber and construction materials along a side fence as “debris.” Reddit threads compiled by insurance researchers describe a similar pattern involving roof algae or moss, sometimes on roofs the homeowners consider perfectly serviceable, triggering a non-renewal notice rather than a request to simply fix the issue.

That specific pattern, a long-standing customer losing coverage over a relatively minor exterior finding, turns up often enough across independent review sites that it’s worth treating as a genuine signal about how Liberty Mutual manages its home insurance book, rather than dismissing it as a handful of unlucky anecdotes. So I went through the available third-party ratings, complaint data, and customer reviews to see what the fuller picture actually looks like.

Liberty Mutual Home Insurance Review (2026)

Best for: Homeowners looking to bundle home and auto insurance.

Pros

- Strong financial stability

- Good bundling discounts

- Nationwide availability

- Standard optional coverages

Cons

- Mixed customer satisfaction

- Complaints about non-renewals

- Claims experience varies

- Limited publicly available pricing

The Company, Briefly

Liberty Mutual is one of the largest homeowners insurers in the country, holding roughly a 7 percent share of the U.S. homeowners insurance market and ranking among the top four or five carriers by market share, depending on the source. Founded in 1912 and headquartered in Boston, it sells policies both directly and through independent and captive agents, and it’s licensed to sell homeowners insurance in nearly every state, with Alaska and California being notable exceptions where it currently doesn’t offer new home policies.

One structural change worth knowing about if you’re shopping for a policy: Liberty Mutual announced in 2025 that it would consolidate its personal insurance lines under a single brand starting in 2026, meaning its longtime subsidiary Safeco is being phased out. Existing Safeco customers are being converted to Liberty Mutual policies with no change to their coverage, agent, or pricing structure as part of that transition.

| Liberty Mutual Quick Facts | |

|---|---|

| Company | Liberty Mutual |

| Founded | 1912 |

| Home Insurance | Yes |

| Auto Bundle | Yes |

| AM Best Rating | A (Excellent) |

| States Available | Most U.S. states |

| Mobile App | Yes |

Financial Strength: Not the Problem

Whatever else this review finds, it isn’t a concern about Liberty Mutual’s ability to pay claims. The company holds an “A” (Excellent) financial strength rating from AM Best, and multiple independent review sites cite consistently high marks from Moody’s and Standard & Poor’s as well. For a company of Liberty Mutual’s size and geographic reach, that combination suggests a real regional catastrophe, a hurricane season or wildfire cluster, is unlikely to threaten the company’s ability to honor valid claims. This part of the picture is about as reassuring as it gets in the insurance industry.

Coverage and Discounts: Standard, With a Few Notable Extras

Liberty Mutual’s home insurance policy includes the standard set of coverages you’d expect from any major carrier: dwelling, other structures, personal property, personal liability, guest medical expenses, and loss-of-use costs if you’re displaced from your home during repairs. It also offers optional add-ons for things like water backup coverage and home systems or appliance breakdown protection.

The discount list is reasonable, if not exceptional. Available discounts include reductions for new or substantially renovated homes, a new roof or roof retrofit, staying claims-free for three to five years depending on the specific discount, getting a quote before your current policy expires, enrolling in autopay, and switching to paperless billing. Bundling home and auto coverage together is where the real savings tend to show up, with Liberty Mutual citing an average savings of roughly $950 per year for customers who bundle, a figure that’s been cited consistently across independent review sites.

Where Liberty Mutual scores less impressively is the sheer breadth of its discount list compared to some competitors, which contributed to a notably lower discount-satisfaction score in at least one recent large-scale consumer survey, discussed in more detail below.

Pricing: A Genuine Blind Spot for Comparison Shoppers

Here’s a detail that surprised me while researching this piece: several major insurance research sites, including outlets that maintain “best homeowners insurance” rankings, explicitly note that they cannot include Liberty Mutual in their rate comparisons because the company doesn’t share its underlying rate data with third-party data providers. That’s a meaningful gap if you’re the type of shopper who likes to see exact side-by-side annual premium comparisons before requesting a quote.

The practical workaround, and the advice several of these same review sites give, is simply to get a direct quote from Liberty Mutual and compare it against two or three competitor quotes for your specific home, rather than relying on any published “average cost” figure, since Liberty Mutual isn’t represented in the data those averages are built from.

Customer Satisfaction: A Split Picture Depending on Which Survey You Trust

This is where Liberty Mutual’s home insurance reviews get genuinely interesting, because different research methodologies produce noticeably different conclusions.

A large 2025 consumer survey conducted by Insure.com, using an independent research firm, found Liberty Mutual scoring well above many competitors on ease of service, tying for the top score in that category, along with solid marks for overall customer satisfaction and policy offerings. Its weakest area in that same survey was claims handling satisfaction, where it scored respectably but still trailed top performers, and its discount satisfaction score was notably lower, reflecting the more limited discount list mentioned earlier.

Set against that, other major review sites, including U.S. News and Insurify, describe Liberty Mutual’s home insurance customer satisfaction as consistently below industry average, citing its exclusion from “best homeowners insurance” rankings specifically due to weak consumer survey performance around claims handling, customer service, and overall value. Insurify goes further, citing average customer ratings of roughly 1 out of 5 stars on both Trustpilot and the Better Business Bureau, driven largely by recurring complaints about slow responsiveness and mishandled claims.

Reconciling these seemingly contradictory findings isn’t actually that difficult once you separate what’s being measured. The more favorable survey data tends to reflect the ordinary, day-to-day experience of policyholders who haven’t had to file a significant claim or go through a renewal dispute. The harsher, complaint-driven data tends to reflect exactly the customers who have, whether that’s a denied claim, a surprise non-renewal, or a steep premium increase. In other words: Liberty Mutual’s home insurance experience appears to be genuinely fine for most people, most of the time, and genuinely frustrating for a meaningful minority during the moments that matter most.

The Complaint Data, in Actual Numbers

The National Association of Insurance Commissioners tracks a complaint index for every licensed insurer, with a baseline score of 1.00 representing the number of complaints expected for a company of that size; anything above that means an insurer is generating more complaints than its market share alone would predict.

According to Bankrate’s analysis of this data, Liberty Mutual’s homeowners insurance complaint index ran well below the industry average from 2022 to 2023, a genuinely good sign during that window. In 2024, however, that complaint index nearly doubled, pushing the company’s score just above the industry baseline for the first time in recent years. Whether that represents a temporary blip or the start of a longer-term trend isn’t yet clear from the available data, but it’s a shift worth watching, particularly for anyone planning to hold a policy with the company for many years rather than just one term.

Reading Between the Lines of the Complaints Themselves

Beyond the raw numbers, the actual text of customer complaints across the Better Business Bureau and other review platforms clusters around a few recurring themes:

Non-renewal after exterior inspections, often citing findings, stored materials, roof algae, minor paint wear, that customers feel were exaggerated or inconsistently applied, particularly striking long-tenured, claims-free customers by surprise.

Steep premium increases at renewal, with several reviewers describing increases in the range of two to three times their previous premium, sometimes without what they felt was a clear or satisfying explanation from customer service.

Claims process friction, including reports of slow response times, difficulty reaching a consistent point of contact, and disputes over coverage for specific types of damage, such as certain water damage scenarios excluded under standard policy terms.

To be fair, the same review platforms also include plenty of positive experiences, homeowners who describe smooth claims handling after storm damage or a burst pipe, and who credit their policy with genuinely saving them from a costly loss. The pattern isn’t that Liberty Mutual fails every customer; it’s that when things go wrong, based on the volume and consistency of complaints, they seem to go wrong in fairly specific, repeatable ways.

Who Should Consider Liberty Mutual?

Liberty Mutual may be a good fit if you:

- Want to bundle home and auto insurance.

- Prefer a large, established insurer.

- Value strong financial stability.

You may want to compare other insurers if you:

- Prioritize top-rated claims satisfaction.

- Have concerns about inspection-related renewals.

- Want the widest range of discounts.

Should You Get a Liberty Mutual Homeowners Quote?

Based on everything above, a fair, non-promotional answer looks something like this: Liberty Mutual is financially sound, offers standard coverage with a handful of useful add-ons, and appears to deliver a genuinely solid day-to-day experience for a meaningful share of its policyholders, particularly around ease of service and initial policy setup. Its bundling discount is worth factoring into any comparison if you already insure a vehicle, and its size and reach mean it’s a viable option in nearly every state outside of Alaska and California.

At the same time, the complaint data and lower-tier customer satisfaction scores from several independent research organizations suggest a real, non-trivial risk of friction specifically around claims and renewal decisions, including the possibility of a non-renewal triggered by an exterior inspection finding that a homeowner may not consider serious. If you do move forward with a Liberty Mutual quote, it’s worth asking directly about the company’s exterior inspection standards and non-renewal criteria before you sign, rather than discovering them for the first time during a renewal cycle years later.

As always, the right insurer depends heavily on your specific home, location, and risk tolerance, and this article isn’t a recommendation for or against any particular purchase. Getting a direct quote from Liberty Mutual, alongside quotes from two or three competitors serving your area, remains the most reliable way to find out whether its coverage and pricing genuinely fit your situation.

How we reviewed

We analyzed customer reviews, complaint data, financial strength ratings, consumer surveys, and insurer information to produce this review.

Conclusion

Liberty Mutual isn’t a universally good or bad choice. It combines strong financial strength and competitive bundling discounts with mixed customer experiences around claims and renewals. Comparing quotes and understanding inspection standards before purchasing can help you decide whether it’s the right fit.

FAQ Suggestions

Liberty Mutual homeowners insurance typically includes dwelling, personal property, liability, additional living expenses, and optional endorsements such as water backup and equipment breakdown coverage.

Liberty Mutual has strong financial strength ratings and offers comprehensive coverage, though customer reviews on claims handling and renewals are mixed.

Some policyholders report non-renewals following exterior property inspections that identified maintenance or property condition concerns.

Yes. Bundling home and auto insurance is one of Liberty Mutual’s largest available discounts.

Eligible discounts may include bundling policies, maintaining a claims-free history, installing a new roof, enrolling in autopay, and choosing paperless billing.

Sources:

• AM Best

• NAIC

• Bankrate

• Insure.com

• Insurify

Leave a Reply